Welcome Event Brings New Neighbours Together

September 13, 2018

Bloomdale’s newest residents were welcomed recently with fun, food and new friends at the Bloomdale Sales & Information Centre. Attendees…

March 7, 2020

When you’ve made the decision to buy, it’s easy to start scouring property websites to find your dream home. But whether you’re thinking about buying an existing property, purchasing land to build on or want a house and land package in a master-planned community, it’s important to prioritise your finances first and foremost.

The main issue buyers make – especially first homeowners – is not realising that the price of the home is not all you’ll pay. From stamp duty to conveyancer fees, it’s easy for an initial budget to blow out. That’s why your first home should cost less than you can afford.

Most generations have an ingrained feeling that your home is an indication of your success. By that logic, bigger is better and more expensive is always best. But that’s not necessarily the best way to look at a property, as it can start you off on the wrong foot and lead to serious financial issues down the track.

Instead of thinking about a house as an impressive notch on your belt, view it as a home. It’s a place where you will spend most of your time, where you will relax after a long week at work, where you might choose to raise a family. Spending above your means just to snag a fancy house with a big price tag doesn’t make it a home.

While the Banking Royal Commission has certainly changed the way lenders are allowed to assess their loan criteria, you’ll probably hear some big numbers when it comes time to get a preapproval.

Your bank or financial provider will use things like your savings, your current income, your job type, your level of debt and any history of defaulting on loans to determine how much you can borrow. The problem is that if you’re unsure exactly how much you want to spend on a home, their suggestions will often sit at the top end of the scale. But that doesn’t mean you should buy a property worth that much.

Think about a couple who make $150,000 a year combined. If the bank approves them for a $750,000 loan at 3% and they spend up to their limit, they will (depending on how much they’ve saved for a deposit) end up paying most of their salary directly into their mortgage over the life of a 30-year loan. That’s not including utility bills, council rates and all the day-to-day living expenses. With those type of numbers, you can see why some Australians are struggling with mortgage repayments and even risking repossession due to buying property for more than they can comfortably afford.

If you fall in love with the price guide of an established home, that doesn’t mean that’s how much it will actually go for. Melbourne, for example, is seeing regular increases in price guides due to so much interest – which is effectively blocking first home buyers out of the bidding war. Then there’s the popularity of auctions which regularly go for tens of thousands of dollars above the reserve price.

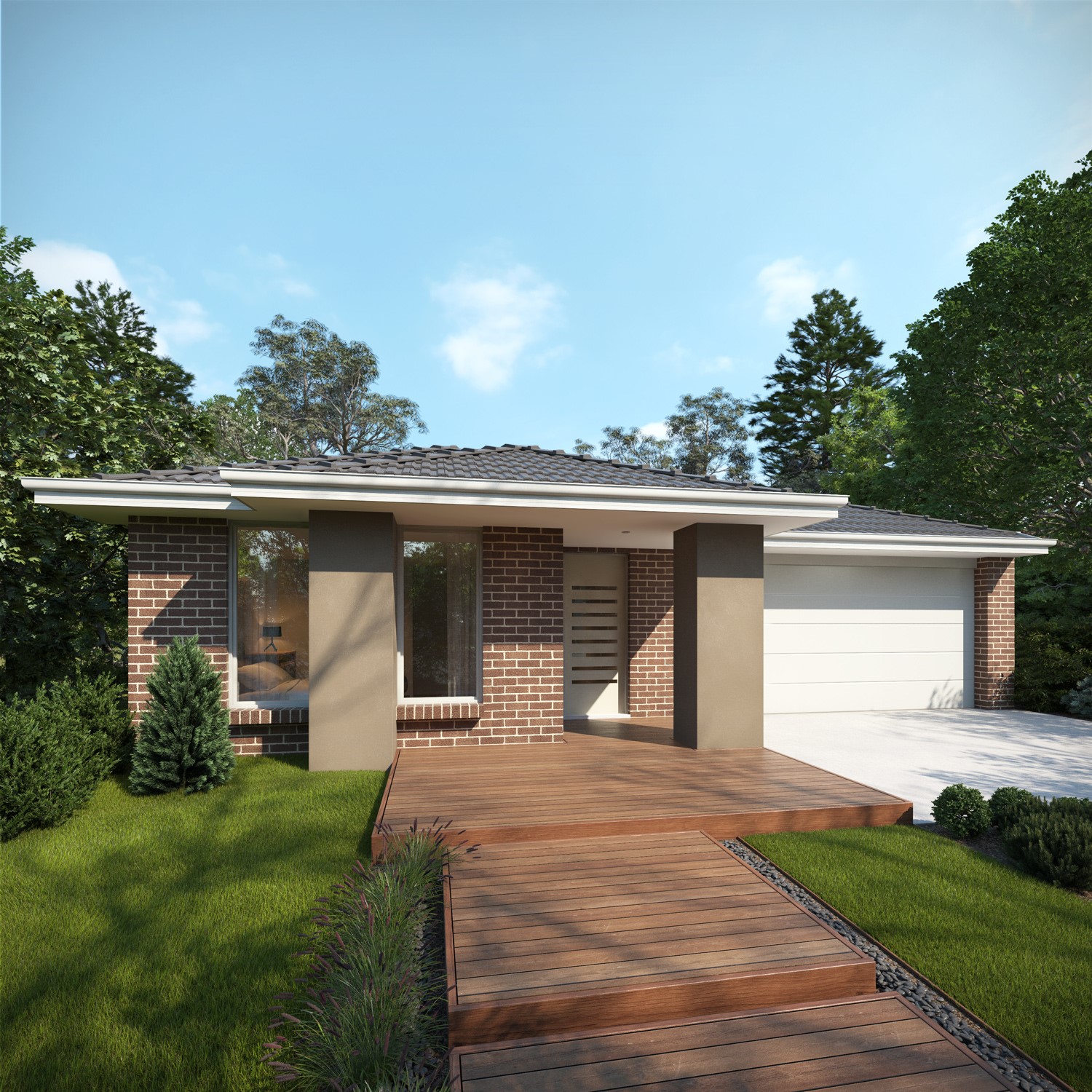

So what’s the alternative? Buying land for sale or purchasing a house and land package in an exceptional master-planned community. Not only do you know the price from the outset, but you’ll get to live in a family-friendly neighbourhood with all the essential amenities at your door – public transport, shopping, entertainment, education facilities, parks and grassland, and so much more.

To experience countryside connected, comfort and contemporary living, as well as the Melbourne CBD just a 30-minute drive away, Bloomdale is the place to be. With a wide choice of block sizes to suit your needs and established facilities at Diggers Rest, you’ll enjoy the life in full bloom, and the convenience of connection from the first moment you enter the community.

Enquire today to find out about house and land packages at Bloomdale.